4/10/25 Recap

The SPY is back below the 8 ema on a big move down after that epic pump yesterday. CPI came in Negative this morning further emphasizing how far behind the curve Powell is at this point with rates. This is just not a healthy market having record volatility and +/- 5% daily moves. The stability of our markets is in question and you’re seeing it in what is now over a week of daily big moves. Yesterday the /NQ was up 2000 today it is down 1200 right now because bonds are getting smashed again. We are just forming an inside day in a series of lower highs, nothing bullish in this chart below for now as the 50 day is about to cross the 200, the “death cross” that you always hear about in the next few sessions. Vix futures are flying right now up over 30% and banks kick off earnings season tomorrow morning.

Today is all about the bond auction at 1 pm, yesterday after I sent out the recap we had one of the craziest moves of all time and closed up the day with the second largest Nasdaq gain ever. The reality is Trump caved, I mentioned in yesterday’s recap that the bond market was beginning to force his hand and even he admitted yesterday he was watching the bond market and decided this was the best route. The reality of the matter is monday the White House said would be no pause and by Wednesday we paused. Look, someone is/was selling treasuries and forcing our rates higher, the who doesn’t matter, but we have a major rate problem now. This entire tariff thing was silly, we literally lit our own house on fire and put out the fire less than a week later and Trump is claiming victory while the 1 country this was all about from the beginning, China, is nowhere near bargaining with us. Hence, today’s big sell off.

I don’t know what happens next but it feels like lower is coming, these China tariffs which are 145% now are going to be a big hit to EPS and to the consumer, I don’t know in what world does anyone think meaningless tariff deals with all these countries ex China is winning. We do have a China problem and it will take a long time to fix it, but hiking tariffs to these extremes in a week, yes they were 54% last week, is just not the solution and the market is telling us as much. We can make deals with every country on earth but without China, the rest are just not very important in the scope of things. Yesterday felt like a bogus relief rally, we had Trump posting on truth social early that it was a great time to buy and then within hours we had a pause on tariffs. Imagine if the CEO of a company dropped a tidbit like that right before releasing materially bullish news hours later, some would say that was illegal.

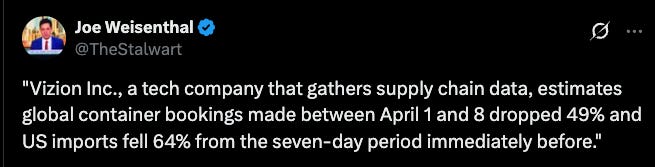

Look, a 15-20% decline in the market is simply pricing in what most see as the likely earnings decline. If we enter a recession the multiple can compress more. Overall I think nothing about yesterday was bullish, even if we make deals with 70 countries, if we don’t make one with China, consumers in America will be impacted negatively in the near term. This morning Andy Jassy was speaking after Amazon sent out their shareholder letter and he mentioned he expects sellers to pass along price hikes, that is inflation, flat out. Nevermind that this morning Joe Weisnthal posted this which shows we’re possibly looking at covid era type shortages in the very near future. Supply shock + price hikes is never a good thing for consumers.

Yesterday appears to have been a president wanting to get the market pressure off him due to the recent market decline and today appears to be market participants realizing how fake yesterday was and resuming the selling. We’re already halfway retracing yesterday’s move and have an even bigger headache ahead as the labor market begins to weaken. What A Mess……

My Open Book