EMERGENCY SESSION: AMAZON

Well I have to do another one of those emergency emails this time late at night like that one recently that came when the market broke trend. I’ve gotten I don’t know how many emails and messages about people in panic right now about the market. META just had a horrible earnings reaction and the overall market has just been in a downtrend for 3 weeks now. I don’t really know what many of you expect, but I’m telling you that many of you are really unrealistic about the market. Markets just move in trends, you go from a long uptrend to a downtrend and back over and over. Where money is made is being in the right names at the right times and that’s my main focus in here sharing option data and insights on names that look interesting to me.

META was down today afterhours on spectacular numbers but they issued some concerns and surprised up on guidance the market sold it off to where it is now only up 20% this year. Think about that, all of you sending me emails are in panic over a stock being up about 6x the market for this year. META is fine, if this move bothered you, you either mistimed it or you had short term calls, that’s it. META will still be $600+ if you want my opinion, probably even higher in say 18 months, they are making tons of money and the small issues will be fixed. Earnings are a complex thing, it really isn’t just about earnings, look at Tesla, they missed on everything and were up because of the optimism. META meanwhile was issuing concerns about China today, the market didn’t like that. I actually was telling someone that last year regarding how great the META numbers were, alot was coming from China and it didn’t seem real to me

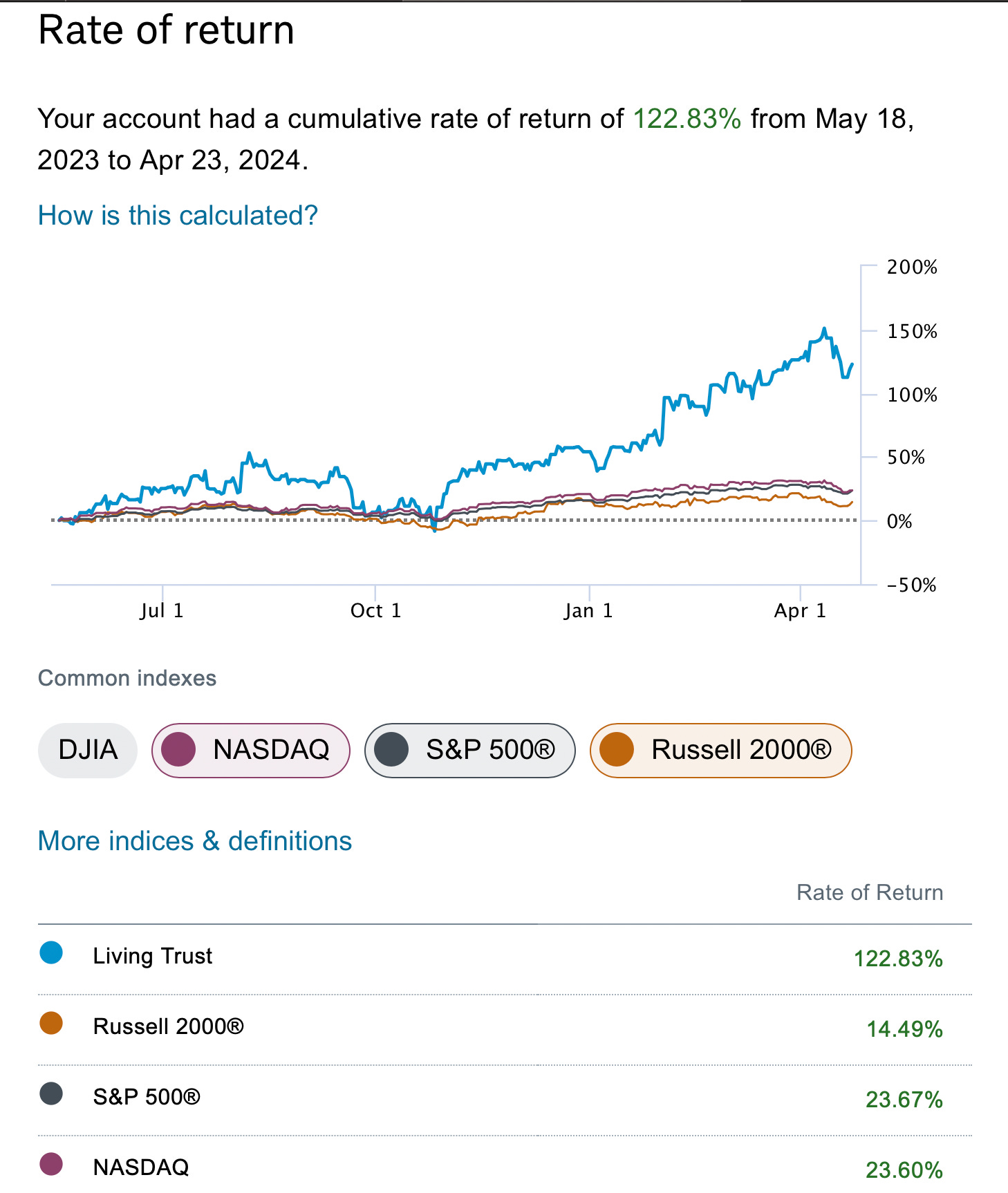

Now we have Amazon earnings are coming up on Tuesday, as you know it is my only position and has been since last May. I know alot of you have a big position and are concerned with the recent move down so I figured I’d discuss it deeper tonight. As for me, it’s been the right trade, regardless of all the ups and downs since I got long calls, the positions is up alot for me. That post came here on May 18th, 2023. Since that time here are my returns, I’m up almost 6x the market, what more do you want me to say.

Am I concerned? No not really, why would I be concerned on a position that expires in June 2026 today in April 2024? Seems silly, anyways I will give you a deeper preview of what I think is coming and where it goes. I will breakdown every segment in depth and tell you what surprises I’m looking for and what negative surprises could come. I spent a long time on this and wrote alot, I hope you enjoy it and this hopefully calms down some of you all.

AWS

I’ll start with AWS because although every analyst on the street sees this as the crown jewel, I personally think it is vastly overrated. This isn’t 2021 where AWS is all of Amazon’s operating income and I am still in the camp that AI is a very overrated thing in its current form. Could AI one day be something big, sure, but for now, the hype cycle is setting the stage for a big disappointment short term. Today Amazon was weak because YIPIT who posted a month back about AWS growth being ahead of schedule and possibly being 16% in Q1 put out a note that AWS was very far behind Azure on AI. Here is the thing, all these analysts who talk about Amazon being behind on cloud are nothing more than a peanut gallery.

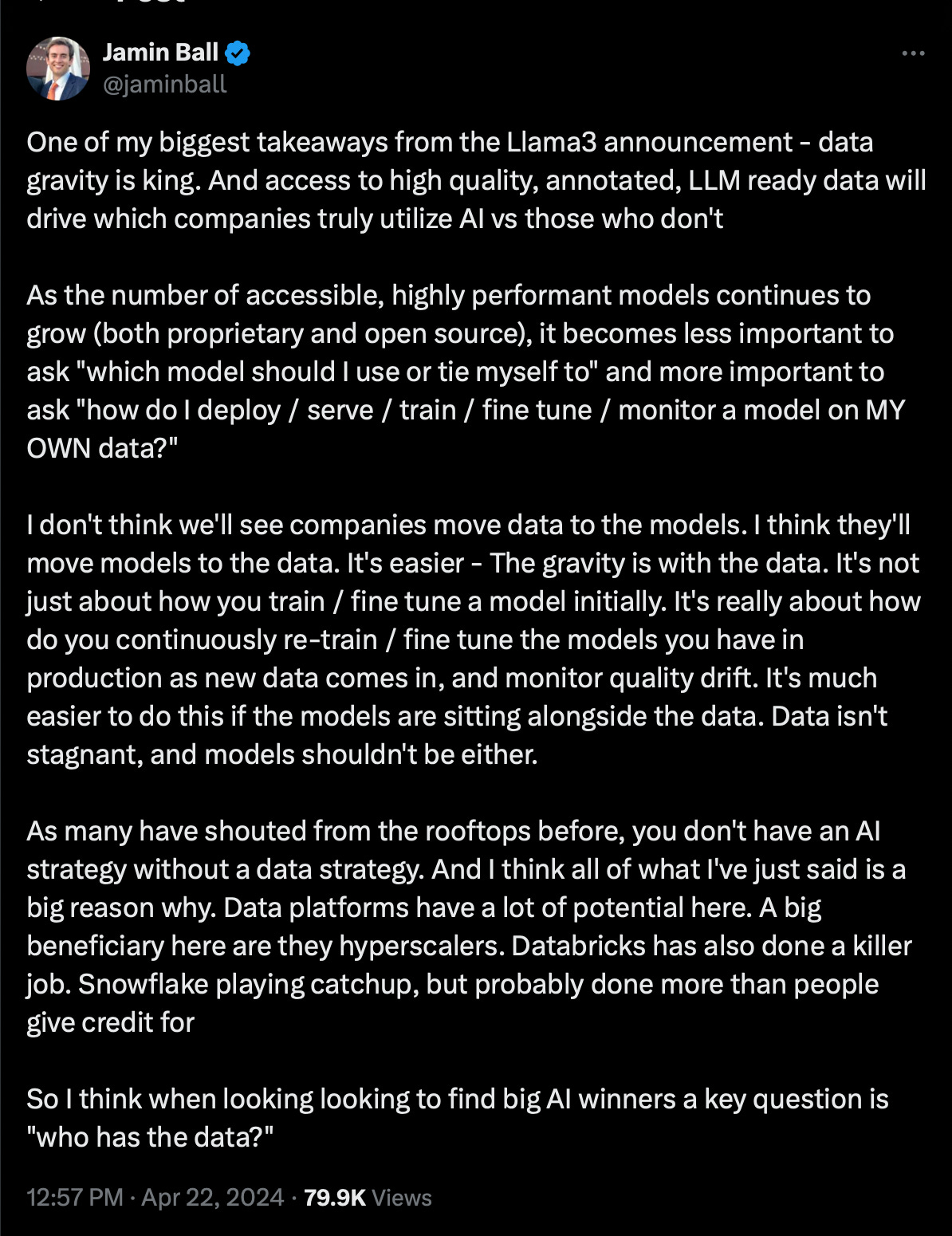

For starters, nobody has more data than AWS and Andy Jassy was the man who pioneered the whole space. Andy has said many times that in the long run he believes people will come to the data and now the other way around. Jamin Ball, a partner at Altimeter said he came to that realization 2 days ago, remember Jassy has said this for a long long time now

Moreover, someone asked Adam Selipsky the AWS CEO late last year about his thoughts on Amazon “being behind” in the AI race and he had a snarky comment asking the host “ Do you know who led search in 1997” and the answer was AltaVista but the point he was making was simply look who leads search today, it really doesn’t matter who leads AI today, it just doesn’t, if this space is as big as everyone seems to think it will be alot will change in the coming years and I don’t see who is better positioned than Amazon to deliver a consumer facing AI product, possibly Apple or Meta.

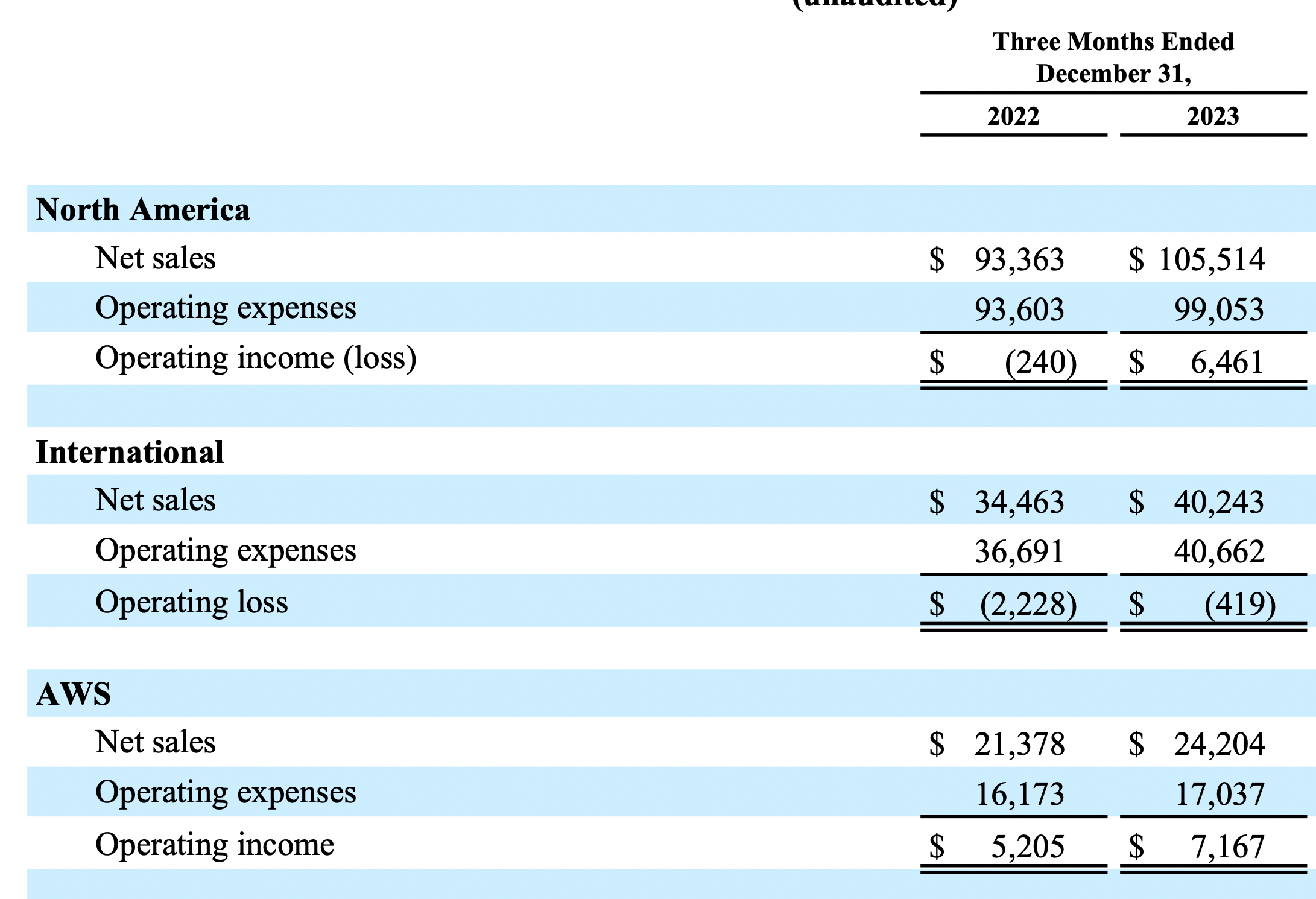

Nonetheless, AWS, as fantastic as it is barely generated $1B more than the rest of Amazon in operating income in Q4 as you can see below. The way everyone discusses AWS, you’d think it was all Amazon had and nothing else mattered. Just ridiculous. At some point this year, I believe the rest of Amazon will overtake AWS on operating income and I think longer term, the TAM of retail at $30 trillion is far greater than the TAM of cloud. Again cloud is a race to the bottom, it’s like payment processors, remember when those were all the rage for investors and now they’re all destroyed? With cloud you’re going to have this massive pie where customers are constantly pushing for lower costs as they solicit bids from others. Retail isn’t that, Amazon has everyone trapped there, they can go to other platforms and lose sales, but if they’re going to sell on Amazon, they’re stuck with Amazon raising fees as they want. Hence why the marketplace business is what I view as the most important business at Amazon. The guesstimates are all over the place here, Mizuho recently said 20% in 2024 which would be a massive acceleration. I don’t know, I would like to see over $24.8B, anything over $25B in Q1 revenue would be amazing. I’d like to see a guide for more and no surprises on AWS Capex guidance for the stock to be happy.

3P

Speaking of the marketplace business, this to me is the world’s most important business. What? James you’re crazy, well as it stands Amazon as a whole is just under 3% of the global TAM of retail sales. Crazy right? As big as Amazon is, a mere 3% of global sales happen on that platform in terms of GMV. With the speed and efficiency they now drive, I don’t know about you, but if I could get every single thing I need on Amazon, I would. It goes back to that question Jeff Bezos posed in his final shareholder letter about “what is your time worth” and he said Amazon saved on average 60 hours a year. So take whatever your hourly income is and multiply it by 60 and then ask yourself is the $139/year fee worth it. That’s an easy yes.

In Q1 last year Amazon did $29.82B in 3P revenue, if they can post another 20% quarter, that would be a big surprise and the market would love it. Amazon is still gaining share from everyone. Temu and the rest are of no concern to me, those are more of a worry for companies focused on low budget people, Amazon is about paying for speed and convenience, those who want to wait 3 weeks for a package can do so on Temu. This business just cranked up fees on sellers dramatically this quarter, it won’t show up in Q1, but they have turned up the dials on sellers and every quarter going forward you will see it. Amazon said for years they were “absorbing” costs and they were and now they’ve offloaded that burden onto sellers and you’re going to see some beautiful margin improvement in q2 on because of it. As for Q1, it is their slowest quarter of the year, I’m sure the numbers will be very good.

Advertising

Ads, this business has come out of nowhere to go from $0 to probably near $60B by the end of 2024 in less than a decade. How many companies can do that? That’s what Amazon does, they constantly find ways to generate more money and now advertising to me is a bigger business than AWS. AWS is at 30% margins and Advertising is much higher. If Amazon does $60B in advertising this year, I think it generates more EBIT than AWS.

This was the first quarter with Prime Video ads. Those began in late January, I expect big things here. META today posted 27% revenue growth mostly all from ads. Last quarter META posted 16% revenue growth and Amazon was at 27%. If this quarter shows similar where Amazon grew ads faster than META then Amazon ads will easily top 30% which is way ahead of where the street is. Amazon will have the highest CPM on streaming ads within 24 months if you want my opinion. Nobody has more data than Amazon on what you buy and that is the most valuable thing to advertisers. Amazon is making big inroads with things like local businesses which never spent money on Amazon video ads, but now they’re all over prime video. Local car dealerships, plumbers, etc that is a whole new segment that Amazon is seeing ad dollars flow from.

On the web, the sponsored ads business is huge and will see plenty of growth as things like their new grocery delivery subscription launched yesterday and there are plenty of sponsored products within that as well. I think advertising will surprise all year long as META had no issues with ad spending today.

Subscriptions

AS I mentioned yesterday Amazon introduced a $9.99/mo subscription for 1 hour grocery delivery, this will likely find many takers with busy professionals who are using Amazon already. They threw in a $4.99/mo subscription for those lower income people on food stamps. Recently they’d added other subscriptions like a monthly fee for Alexa for people who want an emergency call for elderly parents and of course the big one was the $2.99/month they just added for ad free prime video. This alone probably sees very high adoption, I haven’t made the switch yet just because I keep checking out all the various ads, but almost everyone I know has paid that. Just 33 million new users ads $100m/month to Amazon. We don’t know the numbers yet but I imagine they will be very strong

This is the segment that is just a jewel for Amazon. Some companies like Costco, the whole business is valued off subscriptions which pale in comparison to Amazon offerings. Costco is a $320B company right now and Amazon is below $1.8T after the selloff this afternoon. If you want my opinion, it is laughable that Amazon is a mere 6x larger than COST. That’s more how much people overpay for the steady cashflows of COST than anything else. COST is a wonderful company but they don’t have an advertising business nor do they have AWS.

I think a 20%+ increase here would be a big surprise, but with all the advertising subscriptions that came on we may just get that.

1P + Physical

There isn’t much to say here, although nearly half the revenue these segments aren’t that important. They will be fine, but nobody is in Amazon stock for either of them, Amazon is making big optimizations in both.

Cash

Amazon ended last year with just below $90B in cash, by the end of 2026 they will have over $300B in cash. They are the only megacap without a buyback or dividend. They could be initiating one or both this quarter.

Bottom line

I don’t know what Amazon is going to do or say on earnings, nobody knows on any of these earnings. You can have great numbers and say the wrong thing on the call and it tanks, see META today. I do think Amazon is still not fairly valued till probably $220+. From that level, as it grows FCF the stock will follow, I think 30x FCF is a fair multiple for Amazon. I think they surprise and do $75B this year, 30x that is $2.25B and Amazon has over 10.5B shares so that’s my math. I think within 5 years, Amazon will be the world’s largest company and it won’t be close. No company will generate more cash in the coming decade if I was to guess, I feel their stranglehold on retail and consumer shift to e-commerce is not appropriately valued. While other companies like say Google are near max saturation on their main business ie search at over 90% share of global search, Amazon is nowhere near saturation of their main business at 3% of global retail. AWS is also in the early inning if you believe Andy Jassy who says 90% of IT spend is still on prem. I don’t believe it’s that high, but either way all the hyperscalers should see strong growth for years. The media loves to discuss how Amazon growth is slower with no mention it is larger in real dollar terms from a much bigger base.

Amazon isn’t Tesla, they’re not going to make up pump after pump to boost the stock price. Sometimes on these calls you have to have that. It just isn’t their style. They’re not Apple or Google doing buybacks to boost the stock price. Amazon has always been focused on 1 thing, growth at all costs. You can’t even conceptualize the capex that Amazon has spent over the last 3 years at nearly $200b. When people say Amazon doesn’t make money, just ask them where all that Capex comes from. They never have an answer. Amazon has always reinvested in growth and that was fine with everyone during ZIRP, now we’re in this high interest rate environment and investors are demanding profits, that’s fine, Amazon is now showing them and the next few years will see FCF like nobody could have ever imagined.

You have to understand, I don’t really think much of most companies, they’re all just trading instruments to me, up, down, sideways, my goal is to make money with them. Amazon is the only one that I find remotely interesting as a long term investment and I’ve put money where my mouth is because they are the most critical infrastructure company in the world. They’re building things that can’t be upended, that is why Amazon always had the multiple it did while other megacaps like Google were “cheap”. When you think of durability 20 years out, logistics has a much higher probability of existing than Google search which has countless companies attacking it right now. The logistics network will never be built again, when people talk moat, I don’t think any business in the world has a bigger moat than Amazon logistics especially in a world of high interest rates. Even something like AWS, Amazon had a 5-6 year head start on Microsoft because of their lack of pumping. You have some CEO’s like Musk who just let all their competitors know what they’re working on and then act stunned when competition does it better. Amazon knew cloud was a land grab and knew they had to stay silent as long as possible and that’s why they have such a huge lead on Microsoft in that space. So Amazon isn’t the type to come out on these conference calls and just pump things they’re working on, it isn’t their nature. Have you ever heard Jassy mention ZOOX? Most people don't even know what that is, ZOOX has a license to operate a robotaxi in Foster City, California and has for a long time, Amazon owns it and they’re further along in “robotaxi” than Tesla is. You’d never know that because Amazon isn’t going to tell you that, meanwhile Elon Musk is on the call yesterday acting like he’s the first human to think of the concept.

Would I like to see a dividend or buyback? No to the dividend and yes to the buyback. Dividends are a terrible use of capital and buybacks are far more tax efficient. Do I think we get one this quarter? No, I think they want to wait until $100b+ in cash and they’re very close, but the pressure could be on them to do it this quarter. I don’t know we will see but they are bursting at the seams with cash right now and this year is still looking to top $70B in FCF with the bulk of it coming in Q4.

Whatever happens tomorrow, next week, next month, I wouldn’t worry much. This is the other side of the biggest spend cycle in corporate history. Amazon is going to show immense profits, but being so consumer focused and our economy looking like it is heading towards a recession, Amazon is constantly going to be the victim of fears and selloffs. The stock hit all time highs 2 weeks ago and the market has sold off ever since.

This quarterly chart below is about to see the MACD flip positive for the first time in years, if Amazon has a good reaction it could be go time here. I will say this, for the first time in as long as I can remember, Amazon is not reporting on the last Thursday of the month. I don’t know if they didn’t want to report the same day as Microsoft and Google, but is this some subtle hint from Amazon that it is a new era? I don’t want to look into it much but I don’t even remember the last time this happened.

I don’t think any company in our market has a brighter 2 years ahead than Amazon, if Amazon underperforms, then almost everything else will too. The market is barely up this year as of tonight at $172.xx afterhours, Amazon is still up 15% this year, that is a big outperformance, so all of you being dramatic about it are just being ridiculous. Look at the chart below, there is a gap to 160 from last earnings, META filled their last earnings gap today, that is probably a worst case scenario for Amazon. Just remember Amazon is not a 1 trick pony they have 3 major segments that are all doing very well and if AWS could ever pick it up all 3 would be on fire.

Even there it would still be positive for the year. If a 15%+ move off highs is too much for you to stomach, you probably shouldn’t be in tech stocks and you probably shouldn’t be holding calls if you’re doing that. I’m being honest, I don’t even look at account holding my Amazon leaps because what is the point? It’s not like I’m selling them anytime soon, I have 26 months left on these things, unless I hear something materially negative on this call I don’t see why I would change my thoughts on this.

I hope this cleared up many of your fears, I still think this is $220+ by year end, next week who knows, we’re in a downtrend in the market, just maybe try not to have short term calls like I’ve been warning you about for the last few weeks? You will be ok, Amazon will be ok, Tesla will still be a dumpster fire.

Thanks James for your insights. Amazing write up.

Well said and appreciate your analytical thoughts on a wide range of things, such as the comparison of capex cost between companies and why it might not a good idea for Amazon.

Also, on an unrelated topic, and for a future article could you write your thoughts why the 8 ema and 21 ema crossing may signify a market change. Just trying to understand the "why" of it between these two emas.

Thanks, again.